SIP vs LUMP SUM : Choosing the Right Investment Route in Uncertain Markets

Akshay Hedaoo

5/18/20223 min read

SIP vs LUMP SUM : Choosing the Right Investment Route in Uncertain Markets

By Akshay Hedaoo | February 05, 2025 | Founder - Netnium

Investing during market ups and downs can be challenging. When markets are volatile, investors often wonder which approach works better: Systematic Investment Plans (SIPs) or Lump Sum Investments.

Both strategies have unique advantages, but they behave differently in fluctuating markets. This blog will explore how each method responds to volatility and help you decide which suits your financial goals better.

Contents

What is a Systematic Investment Plan (SIP)?

What is a Lump Sum Investment?

How Volatility Affects SIP Returns

How Volatility Affects Lump Sum Returns

SIP vs Lump Sum: A Comparison in Volatile Markets

Conclusion

FAQs

What is a Systematic Investment Plan (SIP)?

A Systematic Investment Plan (SIP) allows you to invest a fixed amount regularly — usually every month — into mutual funds. It follows a method called rupee cost averaging, where you buy more units when prices are low and fewer units when prices are high.

Key Benefits of SIPs:

Makes investing disciplined and consistent

Reduces emotional decision-making

Helps manage market ups and downs over time

Requires a low minimum amount (as low as ₹500 per month)

However, if the market keeps rising steadily, SIPs might buy units at higher prices, which could reduce your overall returns.

What is a Lump Sum Investment?

A lump sum investment is when you invest a large amount of money all at once. This strategy gives you full exposure to the market from day one.

Key Benefits of Lump Sum:

Takes full advantage of rising markets

Ideal when you expect the market to go up

Good for investors who have a large amount ready to invest

However, if the market drops soon after your investment, you could face immediate losses. That’s the main risk of lump sum investing — the timing matters a lot.

How Volatility Affects SIP Returns

In a volatile market, prices keep going up and down quickly. SIPs can benefit from this because of rupee cost averaging:

When prices fall, your SIP buys more units

When prices rise again, those extra units grow in value

This means SIPs may reduce your average cost per unit and give better returns when the market recovers. But if the market stays low for a long time, it might take longer for your investment to grow or break even.

How Volatility Affects Lump Sum Returns

With lump sum investments, your entire amount is at risk from the beginning. If the market drops after you invest, your full amount is affected:

If the market rebounds quickly, lump sum can give high returns

But if the market stays low or fluctuates, it may take time to recover losses

Lump sum investing requires confidence and a long-term view. It works best when the market is expected to grow steadily after your investment.

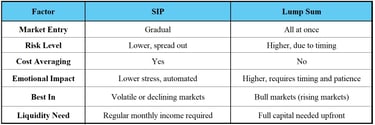

SIP vs Lump Sum: A Comparison in Volatile Markets

Conclusion

Both SIP and lump sum investments have their own strengths and weaknesses in a volatile market. Here’s a quick summary:

SIPs are ideal if you want to invest regularly, avoid timing the market, and reduce the emotional pressure of investing.

Lump sum is suitable if you have a large amount ready and you believe the market will rise in the near future.

There’s no one-size-fits-all answer. Your investment decision should depend on:

Your financial goals

Risk tolerance

Market view

Liquidity needs

You can also combine both strategies — invest a portion as a lump sum and the rest through SIPs to balance risk and opportunity.

Risk Disclaimer:

Investments in mutual funds and stock markets are subject to market risks. Always read the scheme-related documents carefully before investing. Past performance is not a guarantee of future returns. This article is for educational purposes only and should not be taken as financial advice. Consult a certified financial advisor before making investment decisions.

FAQs :

1. What is the minimum SIP amount I can invest?

Most mutual funds allow SIPs starting from RS 500 to RS 1,000 per month. Some platforms may even offer micro-SIPs starting at ₹100.

2. Can I make lump sum investments in parts?

Yes, you can break a large amount into smaller parts and invest gradually. This is called staggered lump sum investing, and it helps reduce timing risk.

3. Is SIP better than lump sum in the long run?

SIPs help you stay invested regularly and handle market ups and downs better. Over the long term, SIPs often deliver stable returns with lower risk. However, in strong bull markets, lump sum investments may outperform.

4. Can I switch from SIP to lump sum later?

Yes, many investors start with SIPs and invest lump sums later when they have more funds or market clarity.

5. Which strategy is safer during market crashes?

SIPs are generally considered safer during crashes because they continue to invest at lower prices, helping lower your average cost over time.